One of the main things to consider when choosing your positions in selling options is the balance between risk and reward. Choosing higher volatility stocks definitely increases your risk to some degree, but also in most cases will have an increased reward through higher premiums. Choosing a strike price that is closer to the current share price when selling a put certainly increases your risk, but there again, it also increases your reward through a higher premium.

Higher risk trades can be offset in most cases by keeping your position sizes small. By doing this, it reduces the stress over a position going against you when you either need to manage the position for a while or in some cases close it out for a loss. If you have to manage a position or two for a while and each of those positions is only 5% or less of your capital, you still have plenty of money to work with.

Keeping plenty of cash available for the downturns is also a way to reduce your overall risk level in a sense. The reason for this is that when the downturns come, you still have money to work with so you can still continue earning premium from selling options.

An Example

Let’s look at an example to illustrate the above concept. In our example say we start with $10,000. Say we were to choose a lower volatility ticker along with a lower delta to reduce the risk of the share price ending up below our strike price at expiration. We’ll use WMT for this example:

WMT current share price is $101.84. For this example we’ll choose an expiration date that is 14 DTE and choose a strike price of $97 which has a delta of -0.17. The premium for selling this put would be $43 or a return of 0.44%. In this case we would be using $9,700 or nearly all of our available $10,000 as collateral for this one position.

Now we’ll compare that to a position where we choose a higher volatility ticker with a higher delta to try and achieve roughly the same premium. We’ll look at the ticker BULL. The current share price is at $11.40. If we sold a put with a 14 DTE expiration at a strike price of $11 which has a delta of -0.40 and implied volatility of about 86% we could collect a premium of $51 or a return of 4.63%. In this case we would be collecting a little higher premium than with the WMT example, but we would only be using 11% of our available capital.

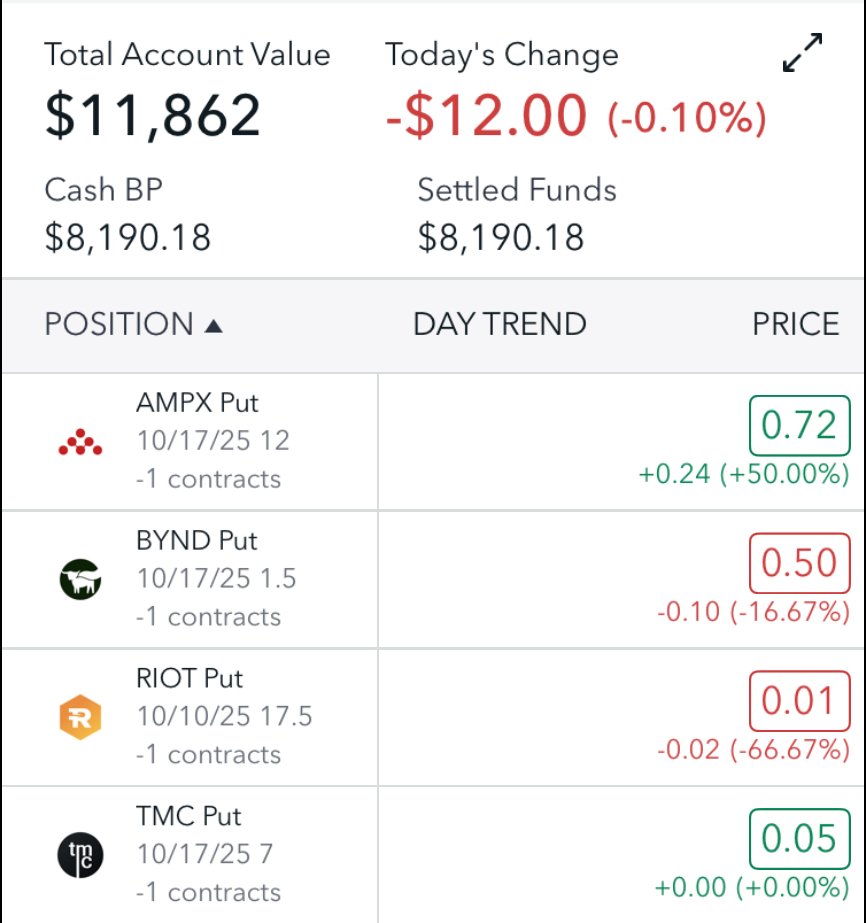

Week 24 Results

These are the put positions that I started the week out with:

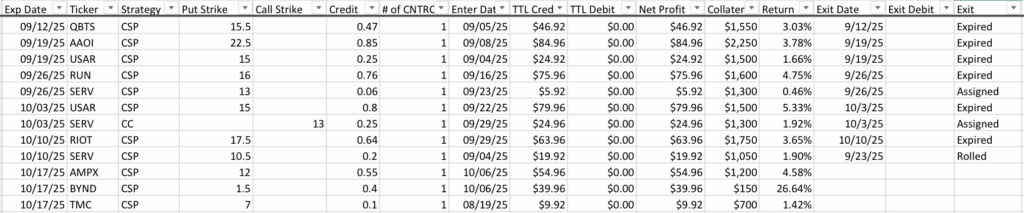

On Monday I opened two new positions. I decided to go with 2 positions with a little lower strike prices mainly to spread the risk out over 2 puts. I opened an AMPX put with an expiration of 10/17 (11 DTE) and a strike price of $12. The premium I collected for this trade was $55.

For my 2nd trade I decided to choose a ticker that had even higher implied volatility than I typically choose. I partly chose this one as it was a much lower share price so my capital put at risk was very low compared to most of my other positions so if the position went against me it would be a very small loss if it got to that point. Of course I was able to collect a much higher premium because of the increased risk percentage wise. This was a put on BYND with a strike price of $1.50 and an expiration date of 10/17 (11 DTE). For this trade I collected a premium of $40.

By the end of the week I was able to let my RIOT put expire. The share price of TMC had also risen even more so things are looking good as of now with this one being able to expire at the end of next week. Here is the chart of my trades since the beginning of September:

Summary

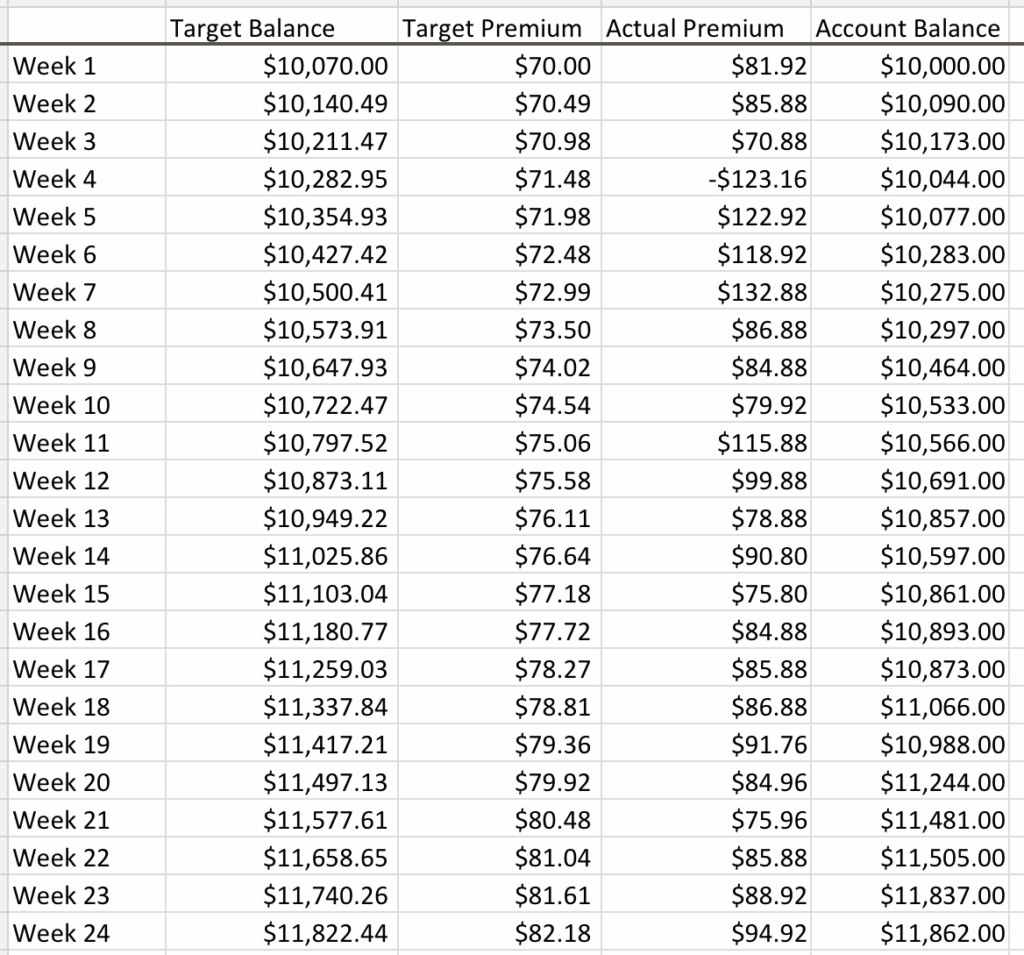

For week 24 I collected $94.92 in net premiums. My target for 24 is $82.18. My total net premiums collected for the first 24 weeks is $1,983.20 (19.83%). The target for my first 24 weeks is $1,822.44. Here is a screenshot of my positions at the end of the week along with the weekly summary: